.svg)

Sometimes mergers and acquisitions (M&A) can feel like juggling a million moving parts—everything from nailing down a fair price to sorting out where the money will come from in the first place. Often, everyone’s so busy zeroing in on traditional financing that they overlook one of the most versatile tools available: seller financing. It’s a simple idea—yet it can completely transform how a deal gets done.

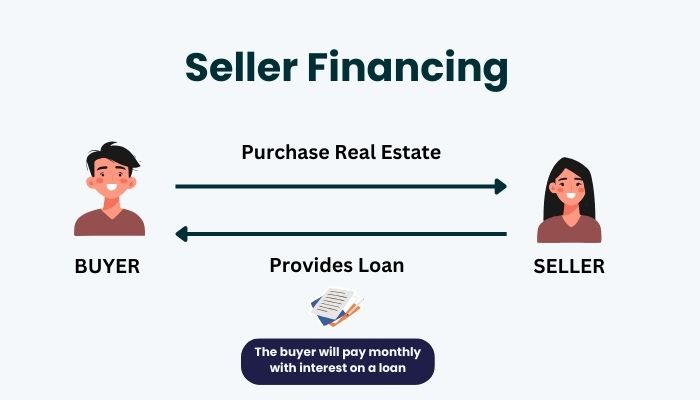

Where Seller Financing Fits In

Picture this scenario: You’re selling your business, and you’re confident it’s worth a tidy sum. The buyer has a strong track record but may not have all the capital (or appetite for big bank loans) to meet your price. Rather than letting the deal stall out, you offer to carry part of the purchase price.In other words, you become the lender for a portion of the total amount. This arrangement can open the door to a smoother negotiation because you’re sharing some of the risk and showing you believe in the future of what you’ve built.

Boosting Trust on Both Sides

In M&A, trust can be just as important as a clean balance sheet. When the seller agrees to finance part of the deal, it signals genuine confidence in the company’s long-term potential—after all, they’re tying some of their payout to how the business performs under new management. From a buyer’s perspective, this vote of confidence can ease worries that the seller is offloading a sinking ship.

Bridging Valuation Gaps

Anyone who’s been through an M&A deal knows that agreeing on a valuation can turn into a tug-of-war. The seller wants top dollar, pointing to all the hard work and goodwill built up over the years. The buyer, meanwhile, wants to hedge against potential slowdowns or uncertainties. Seller financing can break that deadlock.Rather than forcing the buyer to shell out everything upfront (and possibly borrow at steep interest rates), a portion of the purchase price is deferred and paid back over time. This flexibility helps keep the deal alive without forcing either side to compromise on core objectives.

Practical Perks and Pitfalls

- Faster Closings: Because you’re not waiting on lengthy approvals from conventional lenders, deals can close more quickly. Of course, you still need to do proper due diligence, but cutting out extra rounds of bank checks can save precious weeks—or even months.

- Ongoing Relationship: A potential downside is that the seller remains somewhat tied to the business. If the buyer doesn’t manage the company well, repayment could be an issue. Crafting a solid repayment schedule and clear legal documentation can reduce (though never fully eliminate) this risk.

- Win-Win Mindset: Seeing each other as partners—even if it’s only for the repayment period—often leads to a more cooperative transition. The original owner might stick around a bit longer for guidance, helping build relationships with key clients or vendors.

Is It Right for Your Deal?

Not every situation calls for seller financing, but it’s absolutely worth exploring if traditional funding avenues seem constrained or if there’s a real gap between what the seller expects and what the buyer can pay immediately. Before heading down this path, talk with trusted advisors—legal, financial, and M&A experts—to make sure the arrangement is structured properly.At the end of the day, seller financing can be a powerful strategic move. It fosters trust, increases flexibility, and can iron out wrinkles that often derail negotiations. For buyers, it opens doors they might otherwise find locked by strict lending criteria. And for sellers, it’s a chance to tap into the value of their business while still showing faith in its future. When done right, it’s a true meeting of minds that sets everyone up for a stronger, more confident close.

.svg)

.png)

.svg)