.svg)

So, you want to own a business. Maybe you’ve got grand ambitions of becoming the next Henry Kravis, or maybe you just like the idea of using a company’s own cash flow to pay for itself (like an extremely expensive self-licking ice cream cone). Either way, leveraged buyouts (LBOs) are your golden ticket—assuming you don’t mind a little financial acrobatics and a whole lot of debt.

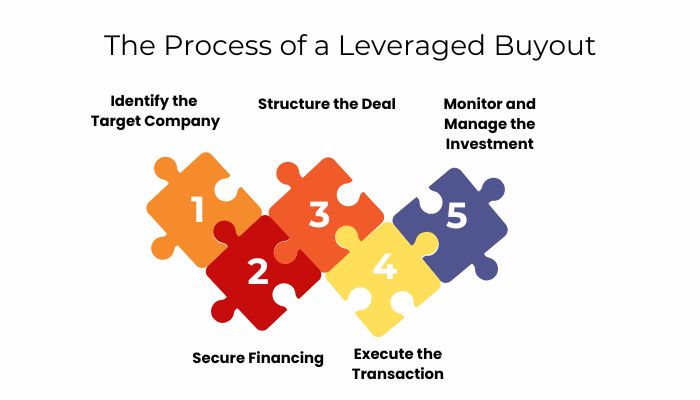

In their simplest form, LBOs involve acquiring a company using borrowed money, typically with the purchased company’s assets serving as collateral. If that sounds risky, congratulations—you’re paying attention. Done right, an LBO is a masterclass in financial engineering. Done wrong, it’s a one-way ticket to Chapter 11.So, how does one actually pull off an LBO? More importantly, how do you do it without becoming the next cautionary tale in financial history? Let’s break it down.

The Mechanics of LBOs – Or, How To Pull Off a Corporate Heist (Legally)

An LBO is essentially the business world’s version of buying a mansion with a tiny down payment and taking out a massive mortgage—except instead of paying that mortgage out of pocket, you convince the house to start earning its own keep.Here’s how the typical deal is structured:

- Equity Contribution: This is the small sliver of actual money you put into the deal, usually from a private equity (PE) firm or other investors. It’s the proverbial "skin in the game," and in LBOs, it’s often as low as 10-30% of the total purchase price.

- Debt Financing: This is the bulk of the deal, comprised of various types of debt (more on this in a second). The goal? Make the company’s future cash flows shoulder the burden while you keep your own capital exposure minimal.

- Target Company Selection: LBO targets are typically cash-flow-rich, undervalued, and a little bloated in the expense department (because PE firms love a good round of “corporate fat-trimming”). You need a business that can handle high leverage while still generating enough free cash flow to service the debt.

Debt Is a Feature, Not a Bug – Until It Is

LBO financing isn't just about borrowing money—it’s about layering debt in the most strategic (and sometimes absurdly complex) way possible.Types of Debt You’ll See in an LBO:

- Senior Debt: This is the safest and cheapest type of financing, often secured against the company's assets. Banks love it because they get paid first if things go south.

- Mezzanine Debt: More expensive than senior debt, but still less risky than pure equity. Comes with higher interest rates and sometimes warrants or equity kickers.

- Subordinated Debt: High risk, high return. The guys holding this paper are basically betting that you’ll pull off your grand strategy instead of running the company into the ground.

- PIK (Payment-in-Kind) Debt: The financial equivalent of "I'll pay you back later." Instead of cash interest payments, the debt accrues over time, creating a lovely little ticking time bomb.

The key to all this debt? EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization)—aka, the number everyone manipulates to make their deal look golden.If EBITDA is strong and growing, your debt load looks manageable. If EBITDA stumbles, well… let’s just say lenders don’t have a sense of humor about missed interest payments.And speaking of stumbling, LBO history is littered with legendary blowups. Remember Toys "R" Us? Great business, but add $5 billion in LBO debt to a shifting retail landscape, and suddenly, Geoffrey the Giraffe was out of a job.

Exit Strategies – Or, How To Flip It and Walk Away Like a Genius

Alright, you’ve bought the business with as little of your own money as possible, loaded it up with debt, and (hopefully) made operational improvements. Now what?There are a few ways to cash out like a pro:

- Sell to Another Buyer: The easiest exit. Find another PE firm or strategic buyer and let them take the debt-laden beast off your hands.

- IPO (Initial Public Offering): Float the company on the stock market, let retail investors bid up the price, and walk away with a hefty return.

- Recapitalization: If the business is doing well, take on new debt to pay yourself a dividend while still keeping control. (Yes, this is as financially aggressive as it sounds.)

But timing is everything. Exit too soon, and you leave money on the table. Wait too long, and you risk the company falling apart before you cash out.

The Ethics (or Lack Thereof) of LBOs – Capitalism’s Favorite Rollercoaster

LBOs get a lot of heat, and for good reason. Are they a brilliant way to create value, or just a convoluted game of pass-the-debt until someone loses? It depends on whom you ask.Common Complaints About LBOs:

- They kill jobs: Cost-cutting is inevitable, and it’s usually employees who get axed first.

- They prioritize short-term gains: PE firms aren’t exactly known for their long-term commitment to businesses.

- They can wreck good companies: If the leverage is too high, even a well-run business can collapse under the weight of interest payments.

But on the flip side, LBOs also create jobs, drive efficiency, and unlock hidden value in companies. Some of the biggest success stories in private equity (Hilton Hotels, Dollar General, etc.) were LBO-driven turnarounds.The bottom line? LBOs aren’t inherently good or bad—they’re just a tool. It’s how you use them that determines whether you’re seen as a financial genius or a corporate villain.

.svg)

.png)

.svg)