.svg)

Mergers and Acquisitions (M&A) deals can be highly profitable, but the key is making sure you understand the details behind investment banking fees.An investment banking fee represents a commission taken by an investment bank, typically based on the size of a proposed transaction. Knowing how to distinguish different fees as well as troubleshoot common misconceptions with these fees is paramount in capitalizing off of successful M&A deals.This article looks to dissect and simplify this industry so that businesses and investors can maximize potential profits through strategic M&A transactions by exploring what these complex fees entail.Factors influencing these charges such as deal size, market conditions, reputability of banks, and fee structures are broken down to offer skilled advice on how to successfully navigate negotiations and potential additional costs, ending in confident leadership decisions regarding these deals.

Types of Investment Banking Fees

1. Advisory Fees

SourceAdvisory Fees are a common form of banking fees for completing Merger & Acquisition (M&A) documents. This type of fee is handled by an investment banker as a retainer during the deal process. Its purpose is to provide operating capital related to securities, and may come in one lump sum payment or more than one installment until desired goal reaches completion.Advisory fees cover not only the cost of the service selected but also compensation for time spent on due diligence reports, drafting business viability assessment recommendations, market pricing evaluation workshops, and preparing valuation reports.It coincides with any negotiation or activity defined under advisory services serviced by the investment banker alongside private lender negotiations if applicable ending issue through successful liquidity stages along all management phases.

Determining Factors

The most common type of Investment Banking Fee in M&A is an Advisory Fee, which is paid for the services offered throughout the deal. Factors to consider when determining this fee include the per-hour rate, total amount expected for labor, and expertise involved alongside project coordination and support needed from employees performing certain duties.Additionally, other affected stakeholders such as tax experts or national regulatory approvals must also be secured in order to complete the proposed transaction on a timely basis.In some cases costs such as travel may need to be stated separately or included within part of a collective fee. Overall when driving towards an agreement make sure that everyone affected is effectively compensated accordingly based upon accepted industry standards and practicalities.

2. Success Fees

SourceSuccess fees, also referred to as “bonuses” or “performance awards,” are an additional form of compensation given to M&A advisory firms once a deal successfully closes. They are aimed at incentivizing investment bankers and their teams to complete complex transactions with successful outcomes.The amount of success fee awarded often revolves around factors such as firm size and scale of the transaction as well as overall importance in driving shares value for all stakeholders or board-specific objectives that may influence total value creation in any M&A transaction.

Calculating Success Fees

Success Fees, also known as commission fees or deal contingent fees, are a form of investment banking fee reserved for deals which result in successful outcomes. Success Fees depend on the size and complexity of the transaction, as well as on the negotiation skills of both parties.These are typically calculated from percentages that have been previously agreed upon by both sides depending on how long it takes for them to make their offers shortly prior to agreement.Due Diligence activities conducted throughout the various merger & acquisition phases should be studied thoroughly before agreeing with any final amount settled for this fee structure.

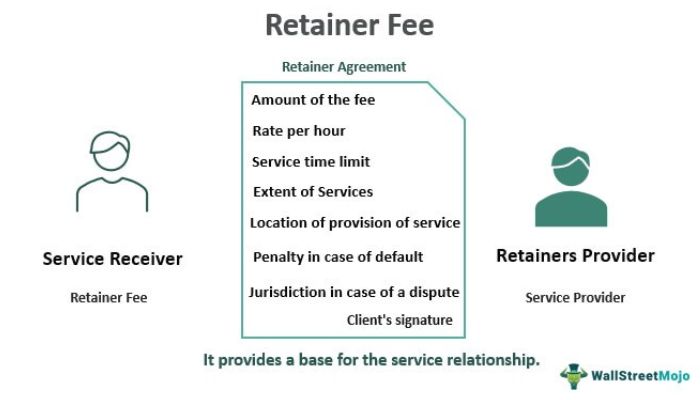

3. Retainer Fees

SourceRetainer fees are generally paid in advance to an investment bank as a type of payment commitment from a business. An effective retainer fee establishes milestones upfront and compensates the investment banker for their work regardless if the deal is successful or not.They’re common practice, especially when a company needs extensive financial work such as value assessments or market strategy development but doesn’t have resources to commit long-term. Usually, ongoing tasks don’t qualify within retainers which encourages the parties to productive results quickly.These fees can also help prevent failed transactions, conflicts of interest or M&A deals being prematurely terminated due to delays and problems arising after consultation with an external advisor.

Advantages and Disadvantages

Retainer fees are engaged when investing banks are needed for financial advising and other services. Their general purpose is to lock in an investment bank’s availability for their services, as well as deter clients from going to rival firms.A retainer fee makes up a large portion of the total bank fees incurred but the advantages of this method also stand out amongst other fee methods: it guarantees undivided attention from a particular banking partner while reducing risk factors with extended direct access and planning help at any given time.The disadvantages which make this approach unique include having to pay up front even if no desired outcome materializes along with a mental cap put on competing parties who partners will not work with during negotiations due to conflict interests related to retainers.

Factors Influencing Investment Banking Fees

Deal Size and Complexity

Deal size and complexity have a direct influence on the cost of investment banking fees. Larger deal sizes typically involve higher levels of due diligence, more complicated filing requirements, and increased expenses for storage, management, scrutineering and documentation.Similarly, more complex transactions such as cross-border M&As can require additional legal provisions to successfully conclude the deal which also drive up costs.Rarely will an investment bank take on definitive tasks without looking at factoring in the financial return associated with it for their services rendered including any consideration or goals laid out ahead of time.

Industry and Market Conditions

Industry and market conditions are key factors influencing investment banking fees. The competitiveness of a target industry can affect the salaries, resources, and other expenses incurred by an investment bank during the deal process.Thus, a slow M&A market with little competition can lower prices whereas high competition will increase rates. Likewise for clients looking to purchase businesses or make investments, more targeted industries come at premium costs compared to less sought out areas.Furthermore, macroeconomic trends can also influence demand in certain sectors due to macroeconomic uncertainty which should be accounted for when evaluating potential fees.

Reputation and Expertise of the Investment Bank

Investment banking fees are determined by several factors including the reputation and expertise of the investment bank. Highly-regarded banks with a lengthy history and extensive market experience will likely charge higher fees than industry newcomers.Additionally, more complex deals such as hostile takeovers may demand larger advisement retainer fees or success awards for reaching a successful transaction completion.Therefore, businesses and investors should be familiar with banks’ quality services within their particular region to be certain they understand all underlying costs that might affect their side of the M&A deal.

Competitive Landscape

The competitive landscape can have a major impact on investment banking fees in mergers and acquisitions. Banks may charge different rates depending on the competition among those offering financial advisory services.That being said, when there are multiple banks bidding for an M&A transaction, that increased competition drives down the fees as each bank tries to outbid the others for promised returns or higher success rates.Moreover, other firms such as private equity groups or family offices competing for business can further alter and influence fees based on their financial capabilities. In some cases, these firms will be willing to concede more lenient terms when acquiring a target company so competition must also be taken into account during negotiations and in determining fee structures.

Fee Structures and Negotiation

Fixed Fee Structure

Fee Structures and Negotiation cover the methods of how investment banking fees are managed from M&A deals. A fixed fee structure is the most common, whereby predetermined payments are agreed upon before the onset of an M&A transaction that cannot be changed regardless of deal outcome or length.This type of fee arrangement promotes trust between brokers and financial institutions involved in a mergers & acquisitions mission by offering everyone a secured outlook on stated earnings.Fees determined this way are also beneficial for business owners as they relieve uncertainty during times of financial excitement, such as when a new venture is transpiring, by providing consistent spending benchmarks from inception to closing.

Transaction-Based Fee Structure

The transaction-based fee structure is an arrangement in which the investment bank’s price is tied to the performance of the transaction. It’s often used as a reward for underwriting, meaning that it exceeds other types of fees more readily and involves variable compensation packages related to outcomes.Whereas fixed fee structures involve predictable costs regardless of transaction results, a transaction-based fee structure will adjust depending on key metrics that could otherwise increase or reduce profits including structuring terms, sale price, and timing of closing among others. Negotiating such an agreement can be daunting but important in order to secure the best deal for all involved parties.

Hybrid Fee Structure

A Hybrid Fee Structure combines elements of both the Fixed Fee Structure and Transaction-Based Fees. In this method, the Investment Bank charges lower fees upfront for their advisory services with higher success fees based on the successful completion of a deal.This type of fee structure allows business owners and investors to benefit from a lowered initial cost while incenting the investment bank to successfully close the mergers or acquisitions for greater remuneration.Negotiating an ideal hybrid fee structure requires knowledge of market conditions and psychology in order to create not only satisfactory terms between both parties but also momentum which leads to skilled negotiation techniques facilitated by both firms throughout the acquisition process.

Tips for Negotiating Investment Banking Fees

In M&A deals, investors and businesses should make an effort to negotiate their investment banking fees for a fairer outcome. Typically, one may start be defining their budget; comparing different fees between various banks, classifying them according to preferences; or including incentive-based structures.Additionally, one may consider negotiating advisory services with a lump sum upfront payment. If applicable, "funneling" up revenue or staged payments can enable better involvement for the bank while reducing fee costs.Distribution of fees among advisors should also be considered when negotiating indirectly with participants in a deal such as lawyers and accountants. Solid communication builds trust strategies which will only benefit both sides of the agreement in the long run.

Additional Costs and Expenses

Reimbursement of Expenses

Reimbursement of expenses is a key additional cost to consider when negotiating investment banking fees for a Merger & Acquisition deal.Generally, an investment bank will seek to be reimbursed for reasonable current and future expenses as this frequently includes travel costs, attorney fees, logistical items, escrow services, and other sundry professional consulting elements.Keeping track of these incurred costs should be accurate and documented through supporting financial data in order to ensure successful disbursal upon the conclusion of the M&A transaction.

Legal and Due Diligence Costs

Legal and due diligence costs are an additional expense that may be associated with investment banking fees. The Legal fees that are related to drawing up and revising contracts, preparing transmittal documents, and providing legal advice or opinion depending on the complexity of the deal.Additionally, due diligence costs refer to the analysis of all material financial data involved with a potential acquisition or merger that is typically performed by the target company’s auditors, appraisers, lawyers, treasurers or other financial advisors. These insights gained from comprehensive research allow for informed decision making processes during M&A negotiations.

Regulatory and Compliance Costs

Regulatory and compliance costs are often an overlooked component of the fees associated with mergers and acquisitions.These additional costs include filing fees, paperwork requirements, travel for meetings, permits, and other administrative touches needed to complete deals. They vary based on information about the deal itself as well as each country’s current regulations.In some cases, these might be passed up by other investors or bankers involved in a transaction. As always, communication is key and all expenses should be examined transparently within M&A negotiations.

Common Misconceptions about Investment Banking Fees

There are some common misconceptions about investment banking fees in mergers and acquisitions. Many feel that the larger the fee charged, the higher quality of service will be provided; this is not necessarily true.Additionally, many think that all banks charge roughly the same rate for a transaction; however, individual firms and banks have distinct fee structures based on their desired compensation as well as aggressive negotiations by buyers or sellers.Lastly, another misconception around these fees is that if they rise significantly during a deal process, it signals something bad with the bank's performance — this may not always be an indication of inferior quality work either since much depends on changing market conditions influencing negotiation dynamics.

Conclusion

The bottom line when it comes to investment banking fees and mergers & acquisitions is transparency and careful negotiation for the best deal that can be achieved. Businesses must understand how these charges are determined, evaluate all alternatives, and research any potential benefits in addition to the fees.Investing in an M&A situation often carries significant transaction costs which could greatly reduce net gains made from a project if unchecked. Thankfully, with preparation and guidance, when negotiated correctly investment banking fees can actually act as a sounding board or tool of property valuation verification protecting investors from unsafe analysis or uninformed decisions while ensuring adequate returns maximize due diligence process outcomes.

.svg)

.png)

.svg)