.svg)

When it comes to mergers and acquisitions, there are two universal truths: buyers want the best deal possible, and sellers want to make their business look like the financial equivalent of a supermodel. Enter EBITDA—earnings before interest, taxes, depreciation, and amortization—the holy grail of valuation metrics that somehow manages to be both revered and misunderstood in equal measure.Of course, the raw EBITDA figure is never quite enough. No, no, we must adjust it, polish it, and inflate it to make it shine. Because nothing says “buy me” like a business whose financials have been creatively, yet totally legally, massaged into something more appealing. But let’s not kid ourselves: adjusting EBITDA isn’t just an exercise in financial prudence—it’s an art form.

EBITDA Funhouse

EBITDA is supposed to represent a company’s true operating performance by stripping away non-operational distractions. The problem? "True operating performance" is about as subjective as modern art. Sellers swear that their EBITDA adjustments are perfectly reasonable, while buyers tend to roll their eyes so hard they nearly detach their retinas.Sellers will claim they’re simply removing distortions—one-time expenses, unnecessary costs, and “non-recurring” charges that, curiously, seem to recur every single year. Meanwhile, buyers know that for every honest adjustment, there’s at least one number that’s been stretched harder than a Silicon Valley startup’s valuation.The truth is, everyone does it. Adjustments are expected. The key is knowing when an EBITDA adjustment is a reflection of reality versus when it’s an outright fantasy.

EBITDA: The Financial Metric Everyone Worships

For all its flaws, EBITDA remains a central figure in M&A. It allows investors to compare businesses across industries without getting bogged down in financing and accounting choices. But let’s be real—many professionals still treat it like some divine number handed down from the heavens, rather than what it really is: a highly manipulatable, often-optimistic estimate of profitability.A company with a rock-solid EBITDA should, in theory, be worth more. But the moment you start making "adjustments," what you’re really doing is trying to convince the buyer that your business is worth even more than that. And why wouldn’t you? After all, it’s not technically lying—it’s just “pro forma” storytelling.

When "Adjusting" Turns Into "Manipulating"

Somewhere along the way, reasonable EBITDA adjustments cross the line into, let’s say, highly optimistic accounting practices. Adjustments start out innocent—maybe you had a one-time lawsuit settlement that skewed your financials. But then you remember that executive bonuses were unusually high last year… and marketing spend was a bit aggressive… and what if we just adjusted for all the inefficiencies the new buyer could hypothetically fix?Before you know it, you’ve adjusted yourself into a valuation that assumes the company will magically operate at peak efficiency under new ownership. Buyers, of course, are not born yesterday. They’ve seen this movie before, and they know exactly what’s happening. But that doesn’t stop sellers from trying their luck.

The Greatest EBITDA Adjustments of All Time

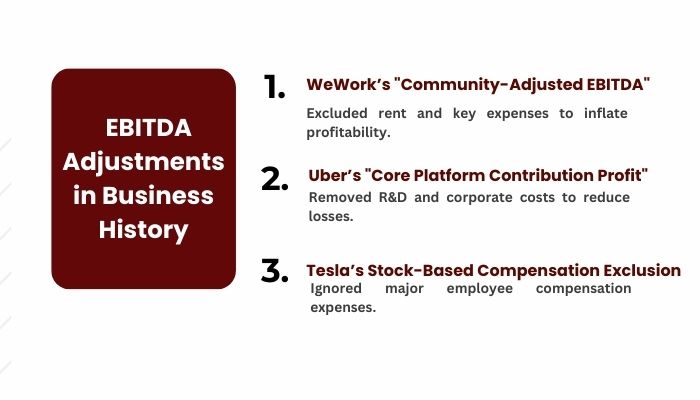

There are a few time-tested, classic EBITDA adjustments that sellers deploy to get their numbers where they need to be. Some are defensible. Others? Not so much.The Classic “One-Time Expense” AdjustmentSellers love to strip out one-time expenses. Legal fees from a big lawsuit? Gone. A major write-off for an unsuccessful product launch? Erased. That massive executive severance package? Oh, don’t worry about that—it’s not part of the “real” business.The problem is that “one-time” expenses have a funny way of happening repeatedly. Any buyer with a functioning calculator knows that while the exact cost may not repeat, something else will inevitably take its place.

The “Owner’s Perks” Adjustment

The moment a seller starts talking about "owner discretionary expenses," you know you're in for some fun. Family vacations classified as "client retreats," luxury cars that were "sales incentives," and let’s not forget about the highly necessary corporate apartment in Aspen.Sure, some of these are legitimate add-backs. But when a seller starts removing everything that made their business look like a well-funded personal expense account, buyers start wondering just how much of the reported revenue was real in the first place.

The Dark Arts of Pro Forma Adjustments

Some sellers don't just adjust past EBITDA—they go a step further. Why stop at reality when you can just invent the financial future? Enter the world of pro forma adjustments, where we don’t just remove inconvenient costs, we also add in hypothetical revenue streams that totally would have happened if we had more time.

“Cost Synergies”

One of the most common tricks in the book is justifying a higher valuation based on "cost synergies." The idea is that under new ownership, the business will operate leaner, smarter, and more efficiently—just ignore the fact that the current management team could have done that but didn’t.

The “We’ll Totally Get That Revenue Boost” Fantasy

Ever heard a seller claim that revenue is about to skyrocket because of a soon-to-be-signed contract? How about an almost-guaranteed expansion into new markets? These are the fun adjustments—where EBITDA isn't just what happened in the past, but what might happen in the future if every single thing goes exactly as planned. Buyers are expected to take this on faith. Spoiler: they don’t.Adjustments Buyers Should Actually Scrutinize Of course, not all EBITDA adjustments are smoke and mirrors. Some actually do make sense. The trick is separating the reasonable from the ridiculous.The “Legit” Adjustments (Yes, Some Exist)Certain adjustments—like removing discontinued product lines or adjusting for seasonal fluctuations—are perfectly rational. No buyer wants to evaluate a business based on revenue streams that no longer exist.

The “Nice Try” Adjustments That Should Set Off Alarm Bells

However, once sellers start adjusting for things like "hypothetical growth" or "temporary inefficiencies" that they just happened to correct right before selling, it's time to start scrutinizing their math. Any adjustment that relies on best-case scenarios rather than past performance should be viewed with extreme skepticism.

Creativity Is Great, But Reality Wins Deals

EBITDA adjustments are a necessary evil in M&A. The trick is knowing when they’re legitimate and when they’re just a clever way to inflate valuation. Sellers will always want to present the best version of their financials, and buyers will always be skeptical.The best deals happen when both sides acknowledge reality—because at the end of the day, no amount of financial acrobatics can survive a serious due diligence process. So go ahead, adjust your EBITDA. Just don’t be surprised when buyers adjust their offers accordingly.

.svg)

.png)

.svg)