.svg)

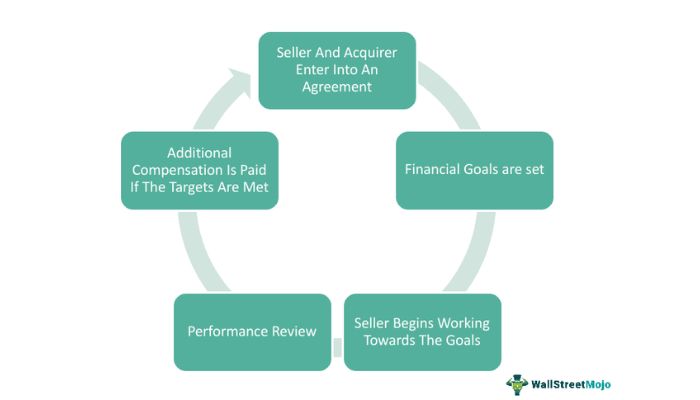

Mergers and acquisitions (M&A) involve complex contractual arrangements, often involving sell-side contingencies in the form of earnouts. An earnout is a payment structure closely associated to M&A that allows sellers to secure larger portions of their final sales proceeds over an extended period.

The advantage of this method is that it adds flexibility to deal structuring which helps mitigate risk for both parties and allows them to take more advantage of potential opportunities for higher valuations.

With active management during post-closing integration time, succeeding with an earnout arrangement can be a great way to align interests and incentives between buyers and sellers in a successful M&A transaction. That said, with new performance targets being taken into mind in such contracts, there are various pitfalls and difficulties associated with honoring an earnout option than at face value.

Benefits of Earnouts

Mitigating Risk for Both Parties

Earnouts are an important tool for managing risk in mergers and acquisitions. By tying future payment obligations or risks to specific performance metrics, both parties can be confident that expected outcomes will be addressed fairly.

Such a contingent obligation arrangement provides participants with increased clarity on the consequences concerning potential circumstances beyond immediate control.

This is particularly beneficial for sellers who seek more secure returns from volatile transaction dynamics, thus ensuring transactions become win-win situations in which maximum mutual gains are secured going forward.

Indeed, with careful planning ahead of time, earnouts help create relationships with lower long term risks mitigating exposure on both sides of any deal between buyers and sellers within mergers and acquisitions.

Aligning Interests and Incentives

Earnouts provide an important incentive for both parties and a way to align their interests. They can give a buyer the ability to offer potentially higher purchase prices without adding uncertainty or taking on additional risk since part of the payment is only triggered by achieving specific financial targets.

The seller’s motivation may then increase its efforts following closing as it has an up-side opportunity via the earnout provisions provided that agreed performance goals and milestones are met over time.

In addition, these structures might encourage both sides of the table to reach successful integration milestones in order to earn out or hit financial objectives faster to extend benefits across all stakeholders sooner rather than later.

Potential for Higher Valuations

Earnouts provide the potential for higher valuations as it incentivizes the sellers to close valuable deals.

The earnout adjusts and/or maximizes total purchase consideration based on the seller’s performance over a defined period of time. When an acquirer uses an earnout, they will be able to pay a lesser amount in cash upfront compared with a traditional sales agreement.

This makes them leery of underestimating numbers whereas sellers benefit from potential gains if their business performs in line with agreed metrics leading towards higher overall valuation upon sale of the company.

Earnouts should also be respected for their ability to create meaningful value for all stakeholders involved in Mergers & Acquisitions transactions monitored judiciously by well-structured agreements.

Pitfalls and Difficulties in Earnouts

Ambiguous Performance Metrics

Pitfalls and difficulties can arise when it comes to navigating earnouts in M&A. One of the most common challenges is determining and setting unambiguous performance metrics which need to be met for the aggrieved party to receive their contractual consideration.

If these performance benchmarks are not clearly stated in the contract with a measurable basis, trust and alignment may be difficult, disputes may arise at a later stage, and claims for remuneration can end up being heavily contested or denied altogether.

Clarity on expectations upfront can thus build consistency across both parties’ interests while minimizing any interpretive ambiguities going forward.

Challenges in Integration and Collaboration

When it comes to earnouts, integration and collaboration can be some of its greatest challengings. Buyers who underestimate the importance of implementing both successful integration and strengthening collaborative efforts during an earnout could miss out on the true value that these types of transactions bring.

- Smoothly integrating willing teams successfully requires immense consideration, including:

- Aligning strategic objectives; effective transition management plans

- Carefully considered performance measures relevant to both parties

- Undertaking thorough due diligence for both companies with litigation risk assessment being a key area in increasing commitment amongst contracted stakeholders

- Staying proactive in monitoring progress against agreed agendas through developing strong lines of communication from inception until exit.

- Disagreements on Targets and Achievements

When it comes to structuring an earnout in merger & acquisition deals, one of the biggest pitfalls is the disagreement between parties on target and achievement metrics. Each party may have vastly differing expectations regarding proposals, thresholds, and performance targets for their project or company.

Furthermore, there can be major differences in approach for how success should be evaluated — depending on price variability criteria, short-term measurements versus long-term actions outlined in the agreement.

Without carefully considered agreements outlining each side’s desired objectives as exactly as possible so that misidentification of critical trigger points can be avoided, successful completion of an earnout arrangement mid-deal is virtually impossible.

Accounting and Financial Reporting Complexities

Pitfalls and Difficulties in Earnouts include complexities from accounting and financial reporting. Defining the relevant key performance indicator (KPI) thresholds for initiating payment to quantify the success or lack thereof of an earnout is difficult due to incorrect anticipation of cash inflows, delays in collecting payment, timing misalignment between goals and different signatories’ commitment on resources, and problems with gaining agreement between auditors on calculation methodologies.

Additionally, the absence of efficient revenue forecasting mechanisms due to considerations with respect to moral hazard may contribute to challenges in recognizing liability and development cost amortization into expenses regularly.

To avoid these disputes along the way it's best practice for stakeholders to anticipate resulting contingencies at every level from paper work drafting stage all through the successful completion of expected returns generation objectives defined therein.

Conclusion

Navigating earnouts in mergers and acquisitions requires considerable care and planning to ensure that both parties can benefit from the arrangement. Merging entities can leverage the potential for higher valuations made possible with a well-structured, risk-mitigating earnout.

At the same time, there are challenges associated with aligning interests and incentives, ambiguities of performance metrics, disagreements over targets achieved, as well complexity such as accounting and financial reporting.

In conclusion, prudent negotiation along with careful craftsmanship of upfront rulebooks is critical to establish clear terms leading to satisfactory agreements by all stakeholders involved while avoiding common pitfalls with transactions using this instrument.

.svg)

.png)

.svg)