If you’ve ever been involved in a mergers and acquisitions (M&A) transaction—whether as a business owner looking to sell, an investor seeking the next hidden gem, or an advisor helping your client navigate the deal process—you’ve probably come across the phrase “DCF model.” You’ve maybe even frowned at the complex financial jargon, the labyrinthine spreadsheet tabs, and the near-endless assumptions.

Some might joke that DCF stands for “Doesn’t Come Free” (referring to the time spent building it) or “Discard and Cross Fingers.” But are DCF models truly outdated, or do they still hold water in the real world of M&A?

In this article, we’ll look at what exactly DCF (Discounted Cash Flow) analysis is, how it fits into M&A transactions, what the critics say, and why—despite the cynicism—this valuation method endures. If you’re deciding whether to trust or toss out DCF in your own deal considerations, read on.

What Exactly Is a DCF Model?

A DCF model is a financial tool that projects a company’s future cash flows and then discounts them back to the present day using a “discount rate,” typically the weighted average cost of capital (WACC). The rationale is that a dollar received tomorrow isn’t quite as valuable as a dollar received today (due to opportunity costs, risk, and inflation). So, by summing all those discounted cash flows plus a projected terminal value, you get a theoretical “intrinsic value” of the business.

If you ask the academics, this is the Holy Grail of valuation. It’s conceptually straightforward, organizes data in a systematic way, and offers a number that’s easily comparable. From that vantage point, DCF is elegantly simple. But once you step into the real world—especially in the complex, fast-paced swirl of an M&A deal—things can get complicated.

Why People Love to Hate DCF

You would think a model revered in MBA classrooms and corporate training sessions would sail into business practice with zero friction. Yet critics often brand DCF as fancy “Excel cosplay” because it can look more like a modeling exercise than a reflection of company reality. For instance:

- Until you realize how assumptions drive outcomes, it’s easy to be mesmerized by the bottom line. A small tweak in growth rates or your discount rate can balloon or deflate your equity value in ways that don’t feel logical.

- Not everything fits neatly on a spreadsheet. Factors like regulatory risk, sudden market disruptions, or brand value sometimes resist tidy numeric classification.

- Many DCFs are built with far-off future projections—five, ten, or even more years down the line—which leads to major guesswork. In dynamic industries, yesterday’s assumptions can become worthless fast.

In an M&A deal, you not only have to convince yourself that your DCF is reflective of reality, but you might also need to persuade buyers, sellers, or other stakeholders. Each party has its own viewpoint—one side may see your DCF as inflated, another as overly pessimistic. Because of how easy it is to manipulate with “what-if” scenarios, some folks dismiss it as more art than science. But the cynical view doesn’t tell the whole story.

DCF Isn’t Just a Math Exercise

When done well, a DCF can force disciplined thinking, especially in an M&A context. Instead of simply throwing a sales multiple or EBITDA multiple at a target without understanding the underlying drivers, a properly prepared DCF ensures you’re pondering the most critical questions about the business:

- How stable is future revenue?

- What’s the company’s sustainable growth rate?

- Are profit margins going to hold, or will competition drive them down?

- How risky is the industry? (which directly informs your discount rate)

In essence, the real value in using a DCF might not necessarily be the final number you spit out but the thoughtful discussion and due diligence that go into building it. If you’re looking to buy or sell a business, that kind of foundational insight can guide negotiations, shape price expectations, and highlight red flags before you commit capital.

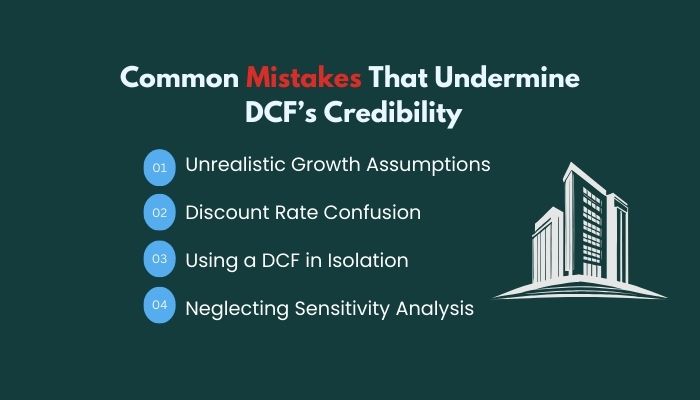

Common Mistakes That Undermine DCF’s Credibility

Critics sometimes see a poorly done DCF and assume the entire method is flawed. But often, the problem isn’t the method; it’s how it’s being used. Here are a few frequent pitfalls that cause eyebrows to roll:

Unrealistic Growth Assumptions

Everyone wants to believe in a bright future, but certain forecasts stretch reality. If you’re anticipating your company’s revenue to grow at 20% year after year—even in a low-growth market—alarm bells should go off. Overly optimistic or pessimistic predictions make the entire model questionable.

Discount Rate Confusion

The discount rate is meant to capture the risk of the projected cash flows. If you select a rate that’s too low, your present value skyrockets; if it’s too high, the value plummets. Many folks either blindly take a default WACC from a textbook or pick a random rate based on vague “market norms.” Neither approach inspires confidence.

Using a DCF in Isolation

A DCF shouldn’t be your only tool for valuation, particularly in M&A deals. Market-based valuation methods (like comparables or precedent transactions) and real-world negotiations help keep your DCF grounded. When you test different approaches and see if the numbers align, you strengthen your valuation perspective.

Neglecting Sensitivity Analysis

If you’re not running sensitivities (changing key assumptions to see how the output shifts), you can end up with a false sense of precision. A well-crafted DCF usually includes a table or scenario analysis that shows what happens if conditions change.

What’s the Role of DCF in M&A Specifically?

In any M&A deal, the buyer is often looking to measure potential synergy, risk, and long-term benefit—while the seller wants to justify the highest possible valuation. The DCF can become a battleground or a peace treaty, depending on how it’s approached.

As a Buyer

You can use a DCF to see if the acquisition price truly reflects the target’s underlying cash-generating potential. It also helps you evaluate how synergy (like cost savings or cross-selling opportunities) might impact overall value.

As a Seller

A DCF can be a powerful narrative device to show your company’s bright future, though, of course, you’ll have to defend your assumptions. Demonstrating plausible figures and telling a growth story can embolden you to ask for a higher price.

In Negotiations

If both sides have their own DCF—fairly common in M&A deals—you can compare assumptions, debate inputs, and hopefully close the gap with a realistic valuation. It can also reveal areas where there’s big disagreement about future prospects, giving everyone a chance to address concerns early.

Beyond the Numbers: What DCF Doesn’t Capture

Even the most thorough DCF will never encapsulate every element that might matter to a buyer or seller. Cultural fit, brand loyalty, intellectual property potential, new industry entrants, or even intangible “gut feelings” can influence the M&A process. That’s why so many professionals see the DCF as part of the puzzle rather than the final solution.

Moreover, in fast-evolving sectors—think tech or biotech—disruptive forces can blow apart carefully crafted models. A promising startup might pivot and skyrocket in value overnight, making a prior DCF irrelevant. In these cases, you might supplement DCF with more forward-looking, scenario-based approaches.

Will DCF Survive the Next Decade?

Despite the jokes and criticisms, DCF is not going anywhere soon. Sure, it can be misused. But at its core, it’s a structure for thinking about future cash generation and the time value of money. In an M&A context, it’s a valuable cross-check, especially when combined with other tools. The real question isn’t whether you should use a DCF, but how carefully and intelligently you’re using it.

Whether you’re in the thick of negotiating a deal or just beginning to explore your options, try approaching a DCF with a dash of realism. Ask yourself whether your assumptions are well-grounded. Seek a second opinion from someone who understands your industry’s unique challenges. Compare your DCF valuation with market-based methods. And, crucially, view it as a conversation starter—a means to test ideas and refine your thinking—rather than the entire conversation.